Stop Waiting for Rates—Here’s the Smarter Move

If you’ve been out looking at homes lately, you already know—affordability hasn’t gotten easier.

So what are buyers doing?

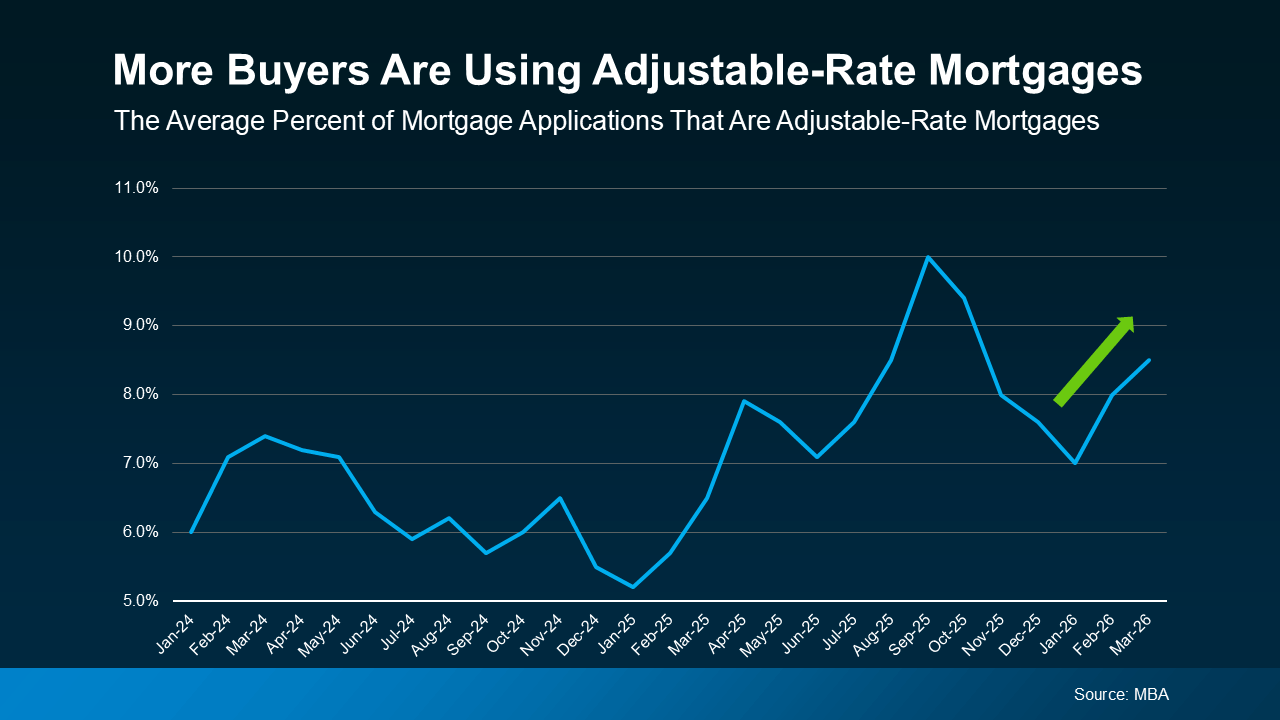

They’re getting creative. And one of the biggest shifts right now is more people looking at adjustable-rate mortgages (ARMs).

Here’s what actually matters.

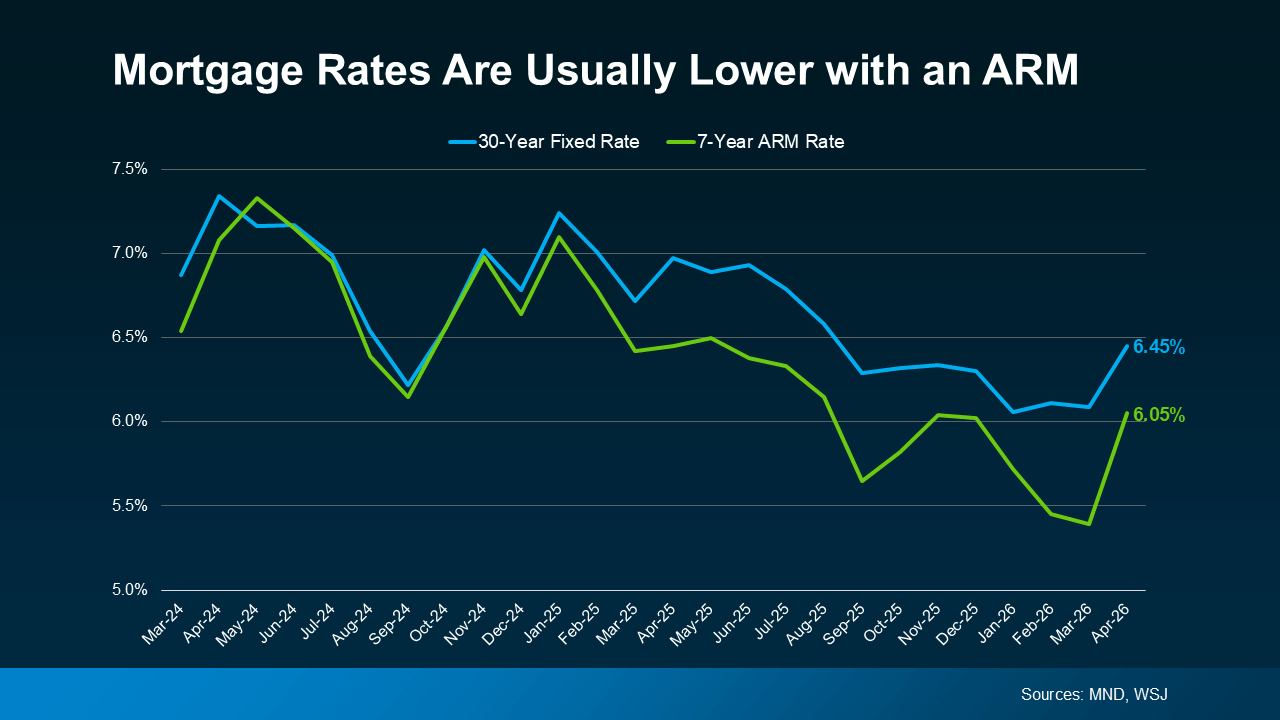

What an ARM Really Is (No Fluff Version)

A fixed-rate mortgage is simple. Your rate stays the same. Your principal and interest payment stays predictable.

An ARM? Different story.

You get a lower rate upfront for a set period—then it adjusts.

That adjustment can go up.

It can go down.

Or it can move enough to make you uncomfortable.

That’s the trade.

Why Buyers Are Moving Toward ARMs Right Now

This isn’t complicated.

Lower payment = more options.

With an ARM, buyers can:

- Reduce their monthly payment

- Stretch into a better home

- Or just make the numbers work in a tough market

We’re seeing real savings—roughly $100–$150/month in many cases.

For some people, that’s the difference between buying and sitting on the sidelines.

Let’s Address the Elephant in the Room

People hear “ARM” and immediately think 2008.

Different world.

Back then, people were getting approved for loans they had no business being in.

Today? Lenders are stress-testing everything.

You don’t get the loan unless you can handle it adjusting.

So no—this isn’t some ticking time bomb.

It’s a tool.

Used right, it works. Used wrong, it hurts.

Where ARMs Actually Make Sense

This is where most people get it wrong—they think it’s about the rate.

It’s not. It’s about your plan.

An ARM can make a lot of sense if:

- You’re not staying in the home long-term

- You expect your income to increase

- You have a clear exit strategy (sell or refinance)

If you’re planting roots for 20+ years and hate uncertainty?

This probably isn’t your move.

The Reality Most People Skip Over

That lower payment today comes with a question mark later.

Rates could be lower when it adjusts.

They could be higher.

Nobody knows.

And if you’re banking on refinancing later—you’re making a bet on the future.

That’s fine. Just call it what it is.

Bottom Line

ARMs are getting more attention because they solve a real problem right now—affordability.

But this isn’t a “one size fits all” move.

This is strategy.

If you’re thinking about it, don’t guess.

Run the numbers. Stress test it. Make sure it fits your plan—not just today, but 3, 5, 7 years out.

That’s how you win this game.

Categories

Recent Posts