Inflation Is Moving the Wrong Way. Here's What It Means for Housing.

If the headlines have you wondering what's happening with inflation, mortgage rates, and the housing market, you're not alone.

If the headlines have you wondering what's happening with inflation, mortgage rates, and the housing market, you're not alone.

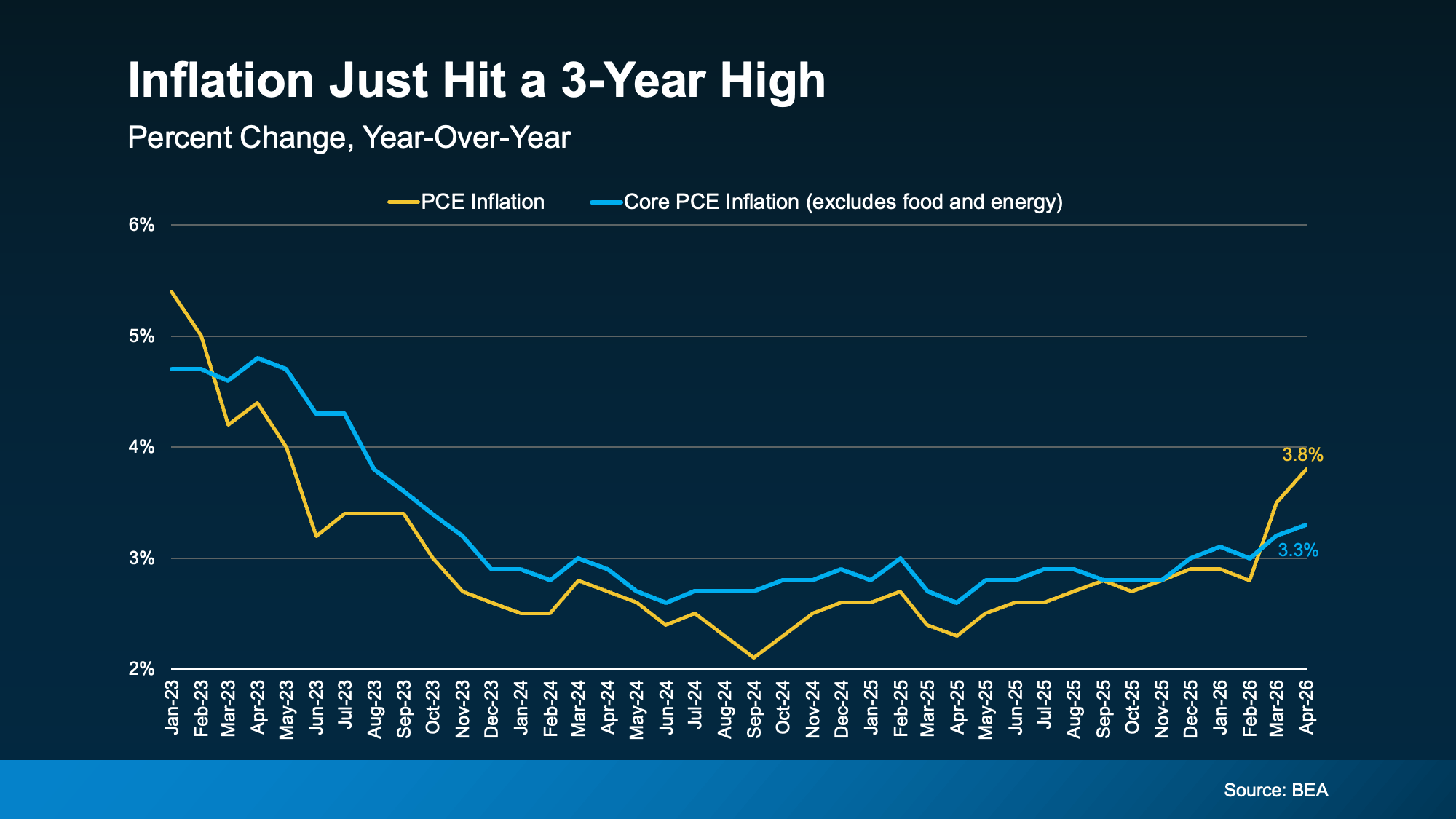

Inflation has been stubborn. While many hoped it would continue moving lower in 2026, recent reports show progress has slowed, and in some cases, reversed course.

Before anyone starts predicting a housing crash, let's talk about what this actually means.

Inflation Matters Because It Influences Interest Rates

One of the biggest things the Federal Reserve watches is inflation.

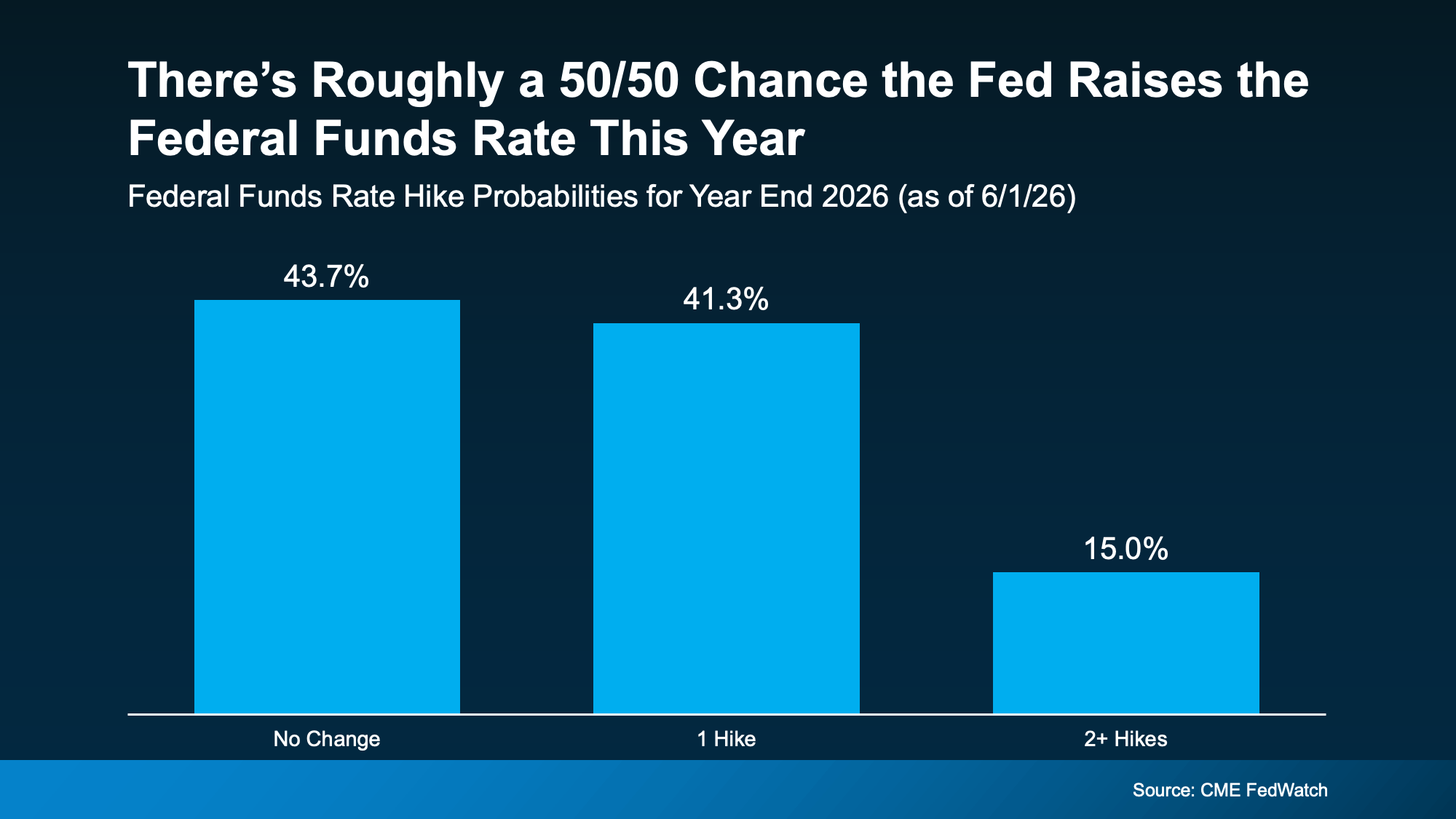

When inflation remains elevated, the Fed is less likely to cut interest rates aggressively. In some situations, they may even consider keeping rates higher for longer.

While mortgage rates don't move in lockstep with the Fed's decisions, inflation is one of the biggest factors influencing where mortgage rates go next.

The reality?

Anyone waiting for a dramatic drop in mortgage rates may be waiting longer than expected.

What This Means for Buyers

Higher rates create affordability challenges. There's no sugarcoating that.

But buyers still have options:

✅ Explore seller concessions

✅ Consider temporary rate buydowns

✅ Look at different loan products

✅ Focus on the monthly payment rather than chasing the perfect interest rate

Many buyers are discovering that waiting for the "perfect market" often means missing opportunities that exist right now.

The best time to buy isn't when rates hit some magic number.

It's when the home, payment, and life circumstances all make sense for you.

What This Means for Sellers

Higher rates have reduced the number of buyers compared to the frenzy of 2021 and 2022.

But serious buyers are still active.

People still get married.

People still get divorced.

Families still grow.

Jobs still change.

Life doesn't stop because mortgage rates are higher.

Homes that are priced correctly and marketed properly continue to attract attention and sell.

This Is Not 2008

One of the biggest misconceptions I continue to hear is that higher rates automatically mean a housing crash.

The data simply doesn't support that conclusion.

Today's market looks very different than it did before the financial crisis:

• Housing inventory remains relatively limited in most markets.

• Homeowners have record amounts of equity.

• Lending standards are significantly stricter.

• Distressed sales remain a small portion of the market.

The challenge today is affordability, not a collapse in housing fundamentals.

Focus on Strategy, Not Headlines

The biggest mistake buyers and sellers make is allowing national headlines to dictate local decisions.

Real estate is personal.

Your goals, timeline, finances, and local market conditions matter far more than a headline designed to generate clicks.

Markets change.

Rates change.

Opportunities come and go.

The people who win are usually the ones who have a plan, not the ones trying to perfectly time the market.

Bottom Line

Inflation remains a challenge, and mortgage rates may stay elevated longer than many hoped.

That doesn't mean the housing market is broken.

It means strategy matters more than ever.

If you're considering buying, selling, refinancing, or simply want to understand what today's market means for your situation, let's have a conversation.

No surprises. Ever.

Categories

Recent Posts