Why This Housing Market Is Stronger Than Most People Think

Everyone loves a housing market disaster headline. The problem? The data doesn't support it.

Everyone loves a housing market disaster headline. The problem? The data doesn't support it.

If you're comparing today's market to 2020 or 2021, then yes, it feels slower. But those years were never normal. Record-low mortgage rates, homes selling in days, and bidding wars on nearly every listing were a once-in-a-generation event—not the standard every market should be measured against.

Compare today's market to almost any other period in modern history, and it's remarkably resilient.

Homeowners Are Stronger Than Ever

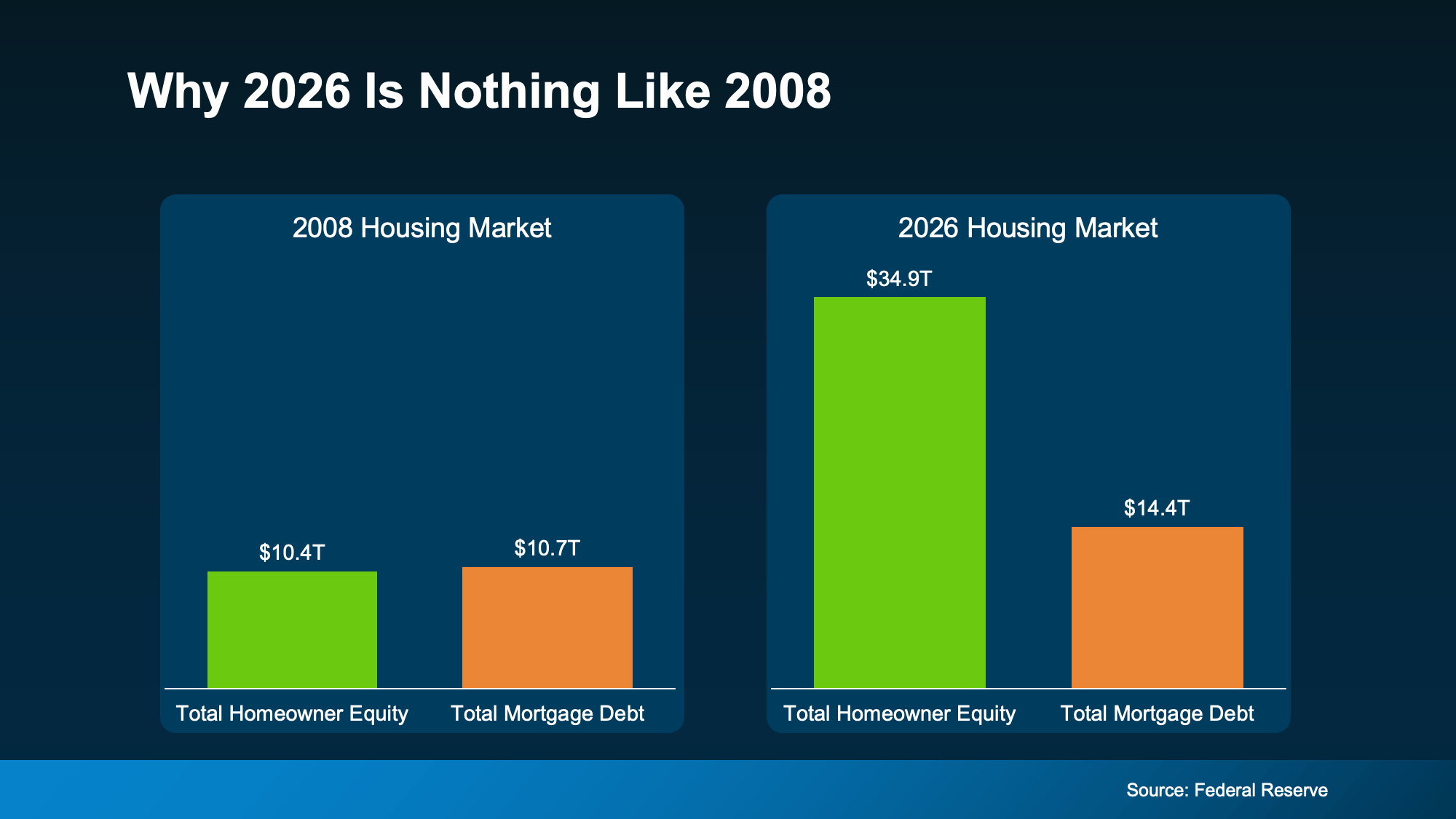

The biggest difference between today and 2008 is simple: equity.

Back then, many homeowners had little or no equity. One financial setback could force a foreclosure.

Today, American homeowners collectively hold roughly $35 trillion in equity. That's an enormous financial cushion.

If life changes and someone needs to sell, most can. They're not trapped. They're selling from a position of strength.

The average homeowner who has owned their home for five years has built around $180,000 in equity. Stay six to ten years, and that number climbs to more than $340,000.

Even more telling, about two-thirds of homeowners either own their home outright or have more than 50% equity.

That's not a market under pressure. That's a market built on solid financial footing.

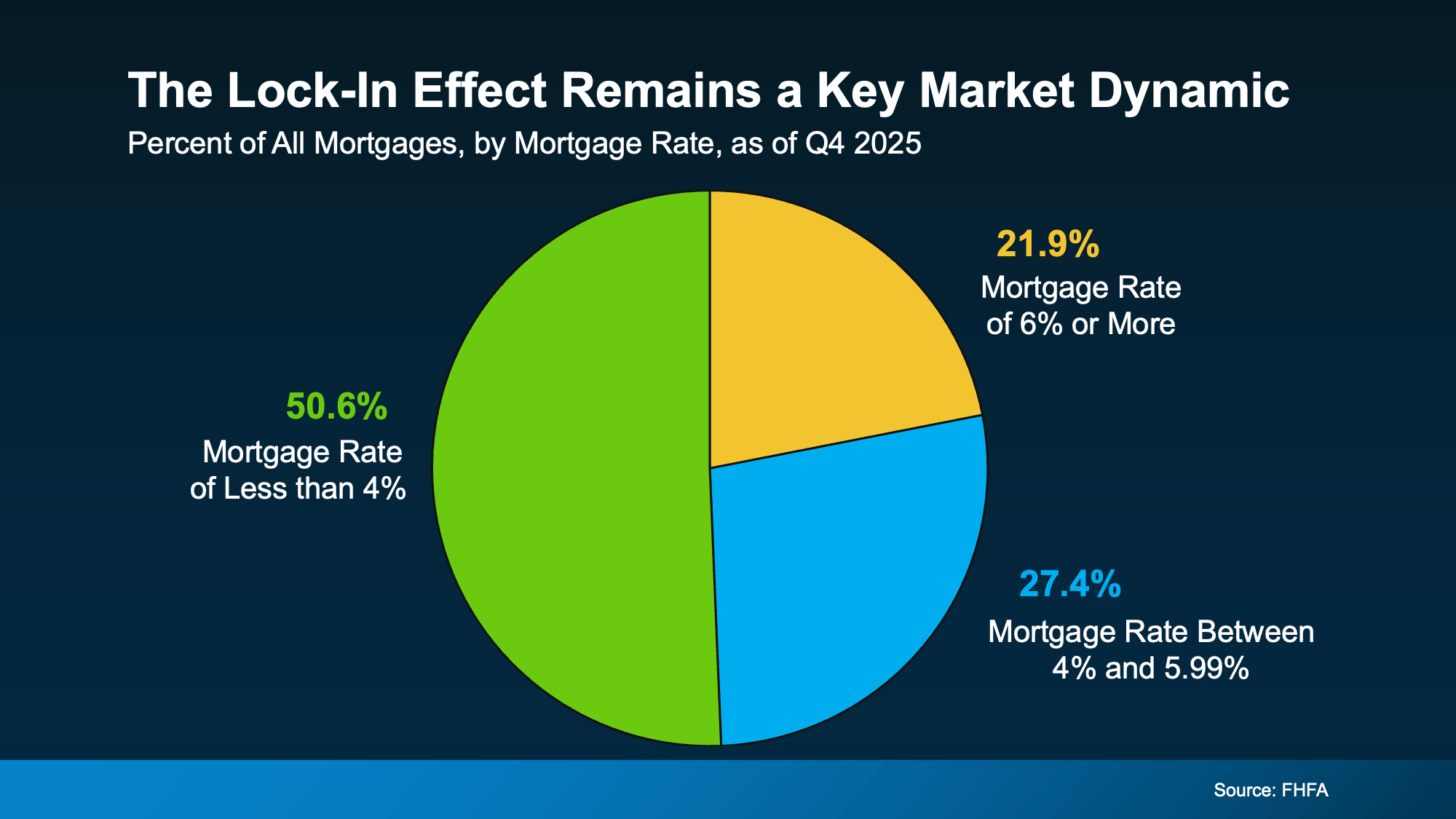

Why Inventory Is Still Tight

People keep asking why more homes aren't hitting the market.

The answer is simple.

More than half of homeowners have mortgage rates below 4%. They're not financially stressed. They're comfortable.

They're not refusing to move because they're scared. They're staying because replacing a 3% mortgage with a 7% mortgage isn't an easy decision.

That keeps inventory lower than many buyers would like, but it also prevents the flood of distressed sales people keep predicting.

Foreclosures have increased slightly from record lows, but they're still nowhere near historical averages.

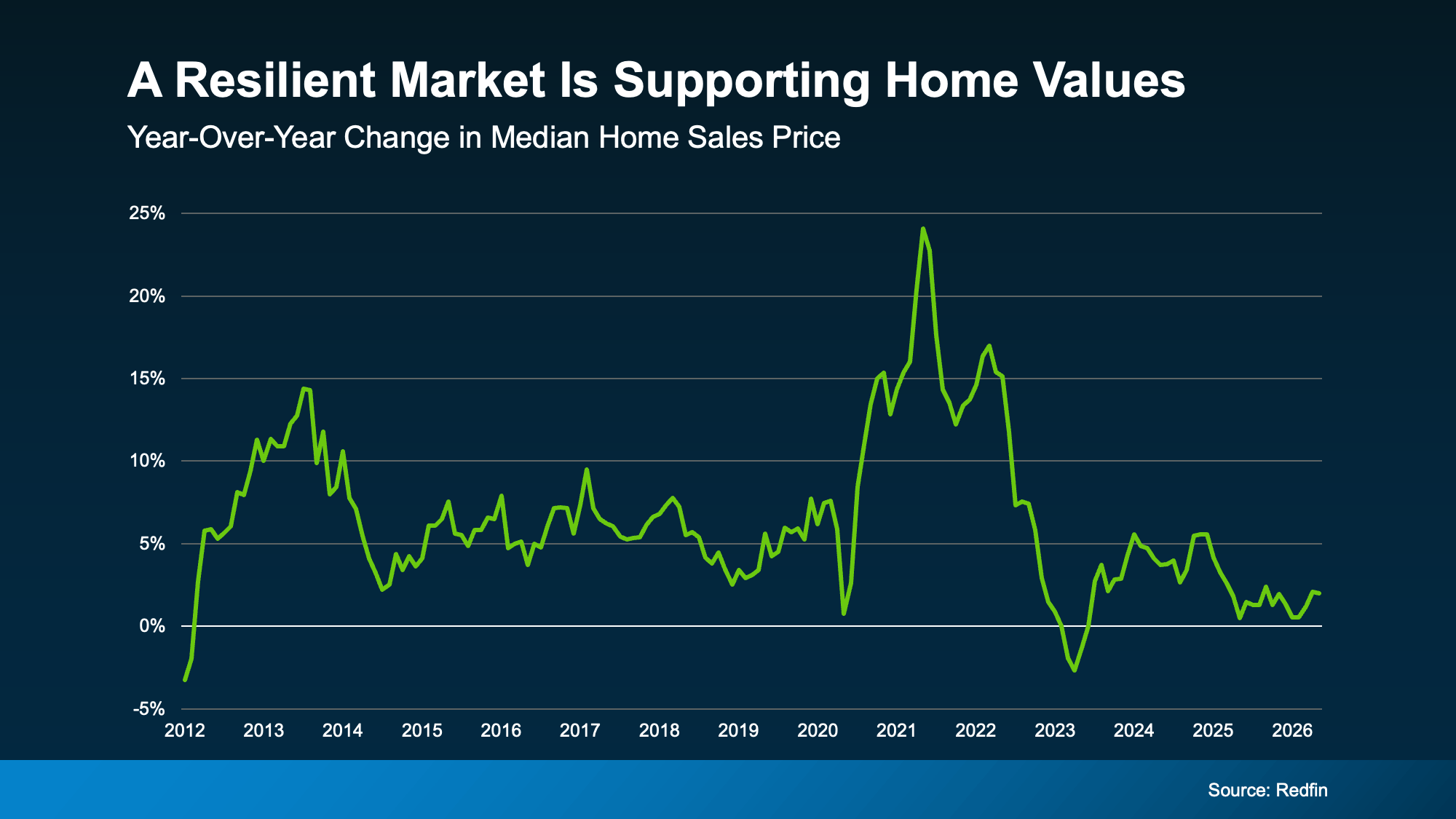

Prices Aren't Crashing

National price growth has slowed to roughly 2% year over year.

That's called normalization.

Markets don't move in straight lines forever. After the frenzy of the pandemic years, slowing appreciation is healthy. It gives buyers more breathing room while homeowners continue building wealth.

A slower market is not the same thing as a collapsing market.

Those are two very different conversations.

The Bottom Line

The people waiting for a 2008-style crash are waiting for conditions that simply don't exist.

Strong homeowner equity.

Historically low foreclosure levels.

Millions of owners locked into low mortgage rates.

That's not the foundation of a housing collapse.

Every month you wait is another month someone else is building equity, negotiating opportunities, and positioning themselves for whatever comes next.

Ignore the headlines.

Pay attention to the data.

Categories

Recent Posts