A Near-Record Number of Sellers Are Pulling Their Homes Off the Market. Should You Be Worried?

You may be hearing that a near-record number of homeowners are pulling their houses off the market. And if that headline has you thinking, "Wait... is something bad about to happen?" you're not alone.

You may be hearing that a near-record number of homeowners are pulling their houses off the market. And if that headline has you thinking, "Wait... is something bad about to happen?" you're not alone.

Because when people start stepping to the sidelines, it can sound like a warning sign. Like sellers know something everyone else doesn't.

But here's the thing: this trend is getting spun like it's proof the housing market is about to crash. And that's not what the data says.

What the Numbers Actually Say

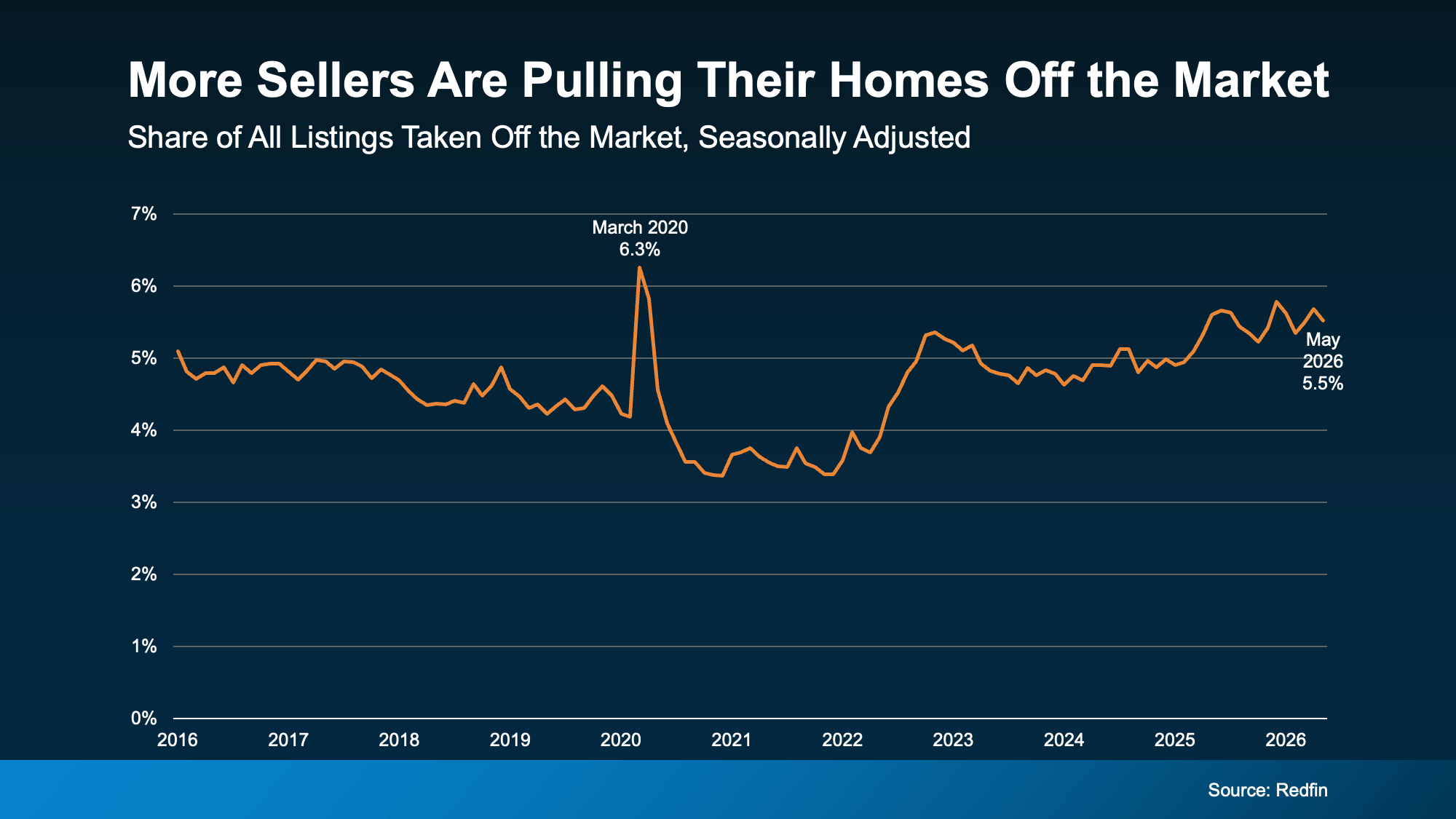

According to the latest data from Redfin, 5.5% of all listings were taken off the market in May. And yes, that's one of the highest levels we've seen since March 2020.

At first glance, that sounds concerning. But a lot of the fear comes from the way the story gets told.

"A near-record number of sellers are pulling their listings" makes a great headline. It grabs attention. It gets clicks. And once it starts circulating online, people naturally assume the worst.

The reality is much less dramatic.

Redfin points to four main reasons more sellers are pulling their homes off the market:

-

Homes are taking longer to sell. Some sellers get frustrated when their house sits longer than expected and decide to wait.

-

Inventory is rising faster than buyer demand. Buyers have more options today, which means more competition among sellers.

-

Some homeowners are still holding onto pandemic-era pricing expectations. What worked a few years ago may not work in today's market.

-

Economic uncertainty is making both buyers and sellers more cautious, slowing down activity overall.

Notice what's missing from that list?

There's no mention of a housing crash. No warning about home prices collapsing. No sign that sellers are running for the exits.

This is a story about a changing market, not a failing one.

The Part Most Headlines Leave Out

Here's another piece of the story that doesn't get nearly as much attention.

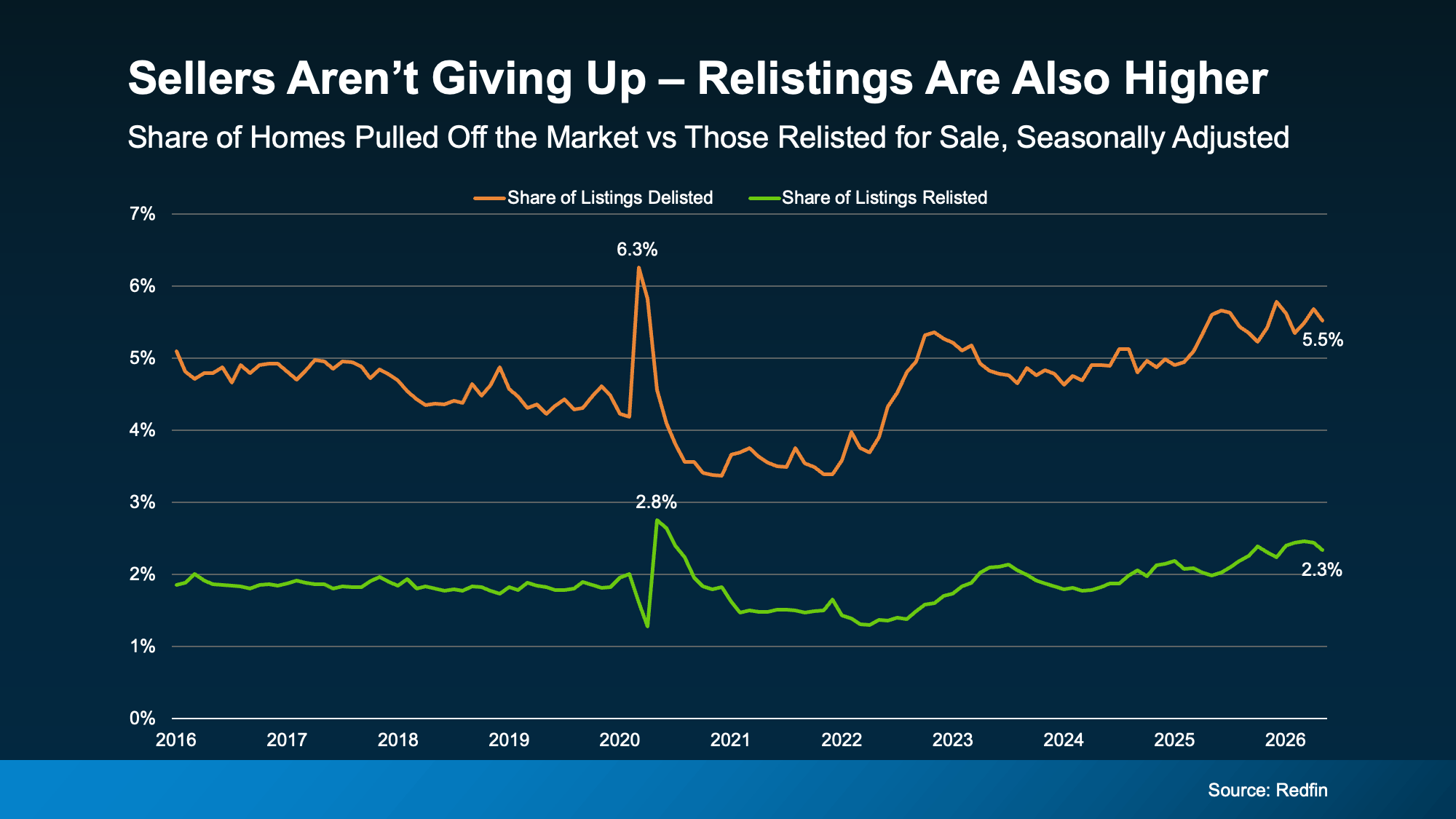

While more sellers are pulling their homes off the market, more sellers are also putting them back on.

In fact, Redfin reports that 2.3% of listings were re-listed in May, one of the highest re-listing rates we've seen since the pandemic.

That's important because it tells us many sellers aren't giving up.

They're pausing.

Maybe they need to adjust their price. Maybe they want to make improvements before trying again. Maybe they're waiting for market conditions to shift.

Whatever the reason, many of these sellers are coming back with a different strategy.

And often, that's all it takes to get a home sold.

Buyer Activity May Be Picking Up Too

If you need even more evidence that this isn't a market-crash story, here's another encouraging sign.

Buyer activity may be starting to rebound.

The National Association of Realtors reports existing-home sales rose 3.2% in May. That's the biggest monthly increase we've seen since December.

As The Wall Street Journal recently put it:

"Home sales in May posted the biggest rise this year, a sign that the housing market's crucial spring selling season may be showing signs of life after a sluggish start."

That doesn't sound like a market that's falling apart.

It sounds like a market that's adjusting, finding balance, and continuing to move forward.

Bottom Line

If you're seeing headlines about a record number of sellers pulling their homes off the market, don't panic.

This isn't a warning sign of an impending crash.

It's a reflection of a market that's changing. Homes are taking longer to sell. Buyers have more choices. Some sellers are adjusting their expectations. And others are simply taking a pause before trying again.

The housing market isn't collapsing.

It's adapting.

Categories

Recent Posts